- Information

- AI Chat

Was this document helpful?

301-Research Memo Example 2

Course: Intermediate Accounting I (ACC 301)

8 Documents

Students shared 8 documents in this course

University: Central Michigan University

Was this document helpful?

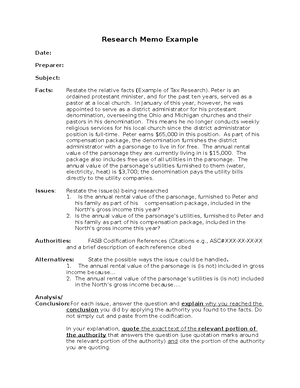

Memorandum

Date: 5/2/21

From: Penny Woelfert

Subject: Period of Revenue Recognition and Persuasive Evidence of Arrangement

Facts: Sales were made to 3 customers at $1 million each with a total $3

million.

All three customers received delivery in December of 2012.

Following normal business practice, Medical Devices prepared, signed

and faxed out sales agreements to each customer in December 2012.

One customer signed and returned the sales agreement on December

29, 2012.

Two customers signed and returned the sales agreements on January 10,

2013.

Issues: Which period(s) should Medical Device recognize $3 million in sales revenue

from sales to three customers who took delivery in December 2012 but signed

sales agreements on January 10, 2013 and December 29, 2012?

Authorities: FASB Codification:

FASB ASC 605-10-25-1

FASB ASC 605-10-25-2

FASB ASC 605-10-S99-1, SAB Topic 13.A.1

FASB ASC 605-10-S99-1, SAB Topic 13.A.2

Alternatives: Alternative 1: Recognize revenue in December for all customers based on

when delivery was made.

Alternative 2: Recognize revenue according to when the contract was signed.

Conclusion: My research indicates the following found under FASB 605-10-S99-1,

SAB Topic 13.A.1-2:

FASB 605-10-S99-1, SAB Topic 13.A.1, Revenue Recognition states:

Revenue generally is realized or realizable and earned when all of the

following criteria are met:

1. Persuasive evidence of an arrangement exists

2. Delivery has occurred or services have been rendered.

3. The seller’s price to the buyer is fixed and determinable.

4. Collectability is reasonably assured.

FASB 605-10-S99-1, SAB Topic 13.A.1, Revenue Recognition expands on

Persuasive evidence of an arrangement as follows:

“FN3 Concepts Statement 2, paragraph 63 states "Representational

faithfulness is correspondence or agreement between a measure or

description and the phenomenon it purports to represent." The staff

believes that evidence of an exchange arrangement must exist to

determine if the accounting treatment represents faithfully the

transaction.”

FASB 605-10-S99-1, SAB Topic 13.A.2, Persuasive Evidence of an Arrangement,

Question 1 refers to a similar situation as Medical Devices Inc. has incurred. The

interpretive Response to Question 1 states that the company discussed had a

business practice of requiring a written sales agreement and as a result,