- Information

- AI Chat

Intermediate Accounting: Contingent Liability and Bonds payable

Intermediate accounting (ACC 205)

Batangas State University

Recommended for you

Related Studylists

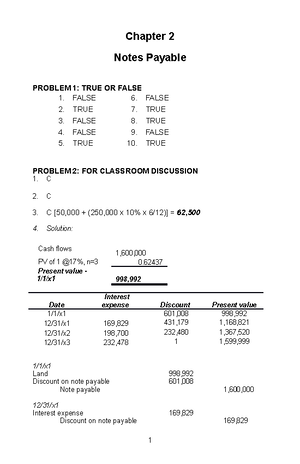

A2Preview text

Colegio de Sto. Domingo de Silos Inc.

Barangay Gulod, Calatagan, Batangas

INTERMEDIATE ACCOUNTING 2

MIDTERM EXAMINATION

NAME: DATE:

SECTION:

INSTRUCTIONS: Select the correct answer for each of the following questions. Mark only one answer for each item by shading the box corresponding to your answer on the answer sheet provided. STRICTLY NO ERASURES. Anyone caught cheating will receive a failing grade or 5 on this subject.

I. TRUE OR FALSE. Write TRUE if the statement is correct and FALSE if the statement is wrong.

- Bond issues that mature in installments are called serial bonds.

- The interest rate written in the terms of the bond indenture is called the effective yield or market rate.

- Amortization of a premium increases bond interest expense, while amortization of a discount decreases bond interest expense.

- If a company plans to retire long-term debt from a bond retirement fund, it should report the debt as current.

- A mortgage bond is referred to as a debenture bond.

- The cash paid for interest will always be greater than interest expense when using effective-interest amortization for a bond.

- Bond issues that mature in installments are called term bonds.

- Premiums are considered as an outright gain of the issuing entity.

- There is a discount when the face amount of the bonds is greater than the its present value.

- Bond issue costs are costs directly attributable to the issue of bonds payable.

II. MULTIPLE CHOICE. Shade the letter of the best answer. 11. The covenants and other terms of the agreement between the issuer of bonds and the lender are set forth in the a. bond indenture. c. registered bond. b. bond debenture. d. bond coupon. 12. The term used for bonds that are unsecured as to principal is a. junk bonds. c. indebenture bonds. b. debenture bonds. d. callable bonds 13. Bonds for which the owners' names are not registered with the issuing corporation are called a. bearer bonds. c. debenture bonds. b. term bonds. d. secured bonds. 14. The interest rate written in the terms of the bond indenture is known as the a. coupon rate. c. stated rate. b. nominal rate. d. coupon rate, nominal rate, or stated rate. 15. The rate of interest actually earned by bondholders is called the a. stated rate. c. effective rate. b. yield rate. d. effective, yield, or market rate. 16. A provision shall be recognized when: a. An entity ha a present obligation b. It is probable that an outflow of resources is required to settle the obligation c. A reliable estimate of the amount of the obligation can be made. d. All of the above. 17. First statement: A contingent liability is a present obligation that arises from past events but is not recognized.

Second statement: Generally, all provisions are contingent. a. True, True c. True, False b. False, False D. False, True 18. It is possible that the company will lose a case under litigation that will lead to possible payment of Php 300,000 to the other party. Should the company recognize a liability? a. Yes, because an outflow of resources is possible. b. Yes because the amount can be measured reliably. c. No, because it is not probable that the case will lose. d. No because the there is no possible outflow of resources. 19. The standards for the accounting of Contingent Liability is under a. PAS 1 c. PFRS 9 b. PAS 37 d. PFRS 27 20. Where the provision being measured involves a large population of items, the obligation is measured using the a. Expected Value c. Regression Analysis b. Mid-point d. Break-even Point 21. Reich, Inc. issued bonds with a maturity amount of $200,000 and a maturity ten years from date of issue. If the bonds were issued at a premium, this indicates that a. the effective yield or market rate of interest exceeded the stated (nominal) rate. b. the nominal rate of interest exceeded the market rate. c. the market and nominal rates coincided. d. no necessary relationship exists between the two rates. 22. An example of an item which is not a liability is a. dividends payable in stock. b. advances from customers on contracts. c. accrued estimated warranty costs. d. the portion of long-term debt due within one year.

- Under the effective-interest method of bond discount or premium amortization, the periodic interest expense is equal to a. the stated (nominal) rate of interest multiplied by the face value of the bonds. b. the market rate of interest multiplied by the face value of the bonds. c. the stated rate multiplied by the beginning-of-period carrying amount of the bonds. d. the market rate multiplied by the beginning-of-period carrying amount of the bonds.

- When the effective-interest method is used to amortize bond premium or discount, the periodic amortization will a. increase if the bonds were issued at a discount. b. decrease if the bonds were issued at a premium. c. increase if the bonds were issued at a premium. d. increase if the bonds were issued at either a discount or a premium. 25 .Theoretically, the costs of issuing bonds could be a. expensed when incurred. b. reported as a reduction of the bond liability. c. debited to a deferred charge account and amortized over the life of the bonds. d. any of these.

- Where there is a continuous range of possible outcomes, and each point in that range is as likely as any other, the _______________ of the range is used to estimate its value of the provision. a. Expected Value c. Regression Analysis b. Mid-point d. Break-even Point

- These are bonds secured by shares and bonds of other corporation a. Mortgage bonds c. Collateral Trust Bonds c. Callable bonds d. Convertible bonds

- These are bonds that can be exchanged for shares of the issuing company. a. Mortgage bonds c. Collateral Trust Bonds c. Callable bonds d. Convertible bonds

- It is the amount printed on the bond.

Notes Payable (3 mo.) 40, Notes Payable (5 yr.) 165, Mortgage Payable ($15,000 due currently) 200, Salaries Payable 18, Taxes Payable (due 3/15 of 2011) 25,

The total long-term liabilities reported on the balance sheet are a. Php 1,865,000 c. Php 1,965,000. b. Php 1,850,000. d. Php 1,950,

On October 1, 2010 Bartley Corporation issued 5%, 10-year bonds with a face value of Php 500,000 at 104. Interest is paid on October 1 and April 1, with any premiums or discounts amortized on a straight-line basis.

- The entry to record the issuance of the bonds would include a a. credit of Php 12 ,500 to interest Payable. b. credit of Php 20,000 to Premium on Bonds Payable. c. credit of Php 480 ,000 to Bonds Payable. d. debit of Php 20,000 to Discount on Bonds Payable. 39 .Bond interest expense reported on the December 31, 2010 income statement of Bartley Corporation would be a. Php 6, 750 c. Php 5, 750 b. Php 11 ,500 d. Php 6, 250

- On January 1, 2010, Huber Co. sold 12% bonds with a face value of Php 600,000. The bonds mature in five years, and interest is paid semiannually on June 30 and December 31. The bonds were sold for Php 646 ,200 to yield 10%. Using the effective-interest method of amortization, interest expense for 2010 is a. Php 60,000 c. Php 64 ,62 0 b. Php 64 ,436 d. Php 72 ,

On January 1, 2020, Ellison Co. issued eight-year bonds with a face value of Php 1,000,000 and a stated interest rate of 6%, payable semiannually on June 30 and December 31. The bonds were sold to yield 8%. Table values are:

Present value of 1 for 8 periods at 6% ..................................................... Present value of 1 for 8 periods at 8% ..................................................... Present value of 1 for 16 periods at 3% ................................................... Present value of 1 for 16 periods at 4% ................................................... Present value of annuity for 8 periods at 6% ........................................... 6. Present value of annuity for 8 periods at 8% ........................................... 5. Present value of annuity for 16 periods at 3% ......................................... 12. Present value of annuity for 16 periods at 4% ......................................... 11.

The present value of the principal is a. Php 534,000. c. Php 623,000. b. Php 540,000. d. Php 627,000.

The present value of the interest is a. Php 344,820. c. Php 372,600. b. Php 349,560. d. Php 376,830.

The issue price of the bonds is a. Php 883,560. c. Php 889,560. b. Php 884,820. d. Php 999,600.

On October 1, 2020 Macklin Corporation issued 5%, 10-year bonds with a face value of Php 1,000,000 at 104. Interest is paid on October 1 and April 1, with any premiums or discounts amortized on a straight-line basis.

The entry to record the issuance of the bonds would include a credit of a. Php 25,000 to interest Payable. b. Php 40,000 to Discount on Bonds Payable. c. Php 960,000 to Bonds Payable. d. Php 40,000 to Premium on Bonds Payable.

Bond interest expense reported on the December 31, 2020 income statement of Macklin Corporation would be a. Php 11,500 c. Php 13, b. Php 12,500 d. Php 23,

46 .A company issues Php 20,000,000, 7%, 20-year bonds to yield 8% on January 1, 20 10. Interest is paid on June 30 and December 31. The proceeds from the bonds are Php 19,604,145. What is interest expense for 2011, using effective-interest amortization? a. Php 1,540, b. Php 1,560, c. Php 1,569, d. Php 1,579,

A company issues Php 5,000,000, 7%, 20-year bonds to yield 8% on January 1, 2010. Interest is paid on June 30 and December 31. The proceeds from the bonds are Php 4,901,036. Using effective-interest amortization, how much interest expense will be recognized in 20 10? a. Php 195, b. Php 390, c. Php 392, d. Php 392,

A company issues Php 5,000,000, 7%, 20-year bonds to yield 8% on January 1, 2010. Interest is paid on June 30 and December 31. The proceeds from the bonds are Php 4,901,036. Using effective-interest amortization, what will the carrying value of the bonds be on the December 31, 2010 balance sheet? a. Php 4,903, b. Php 5,000, c. Php 4,906, d. Php 4,902,

A company issues Php 5,000,000, 7%, 20-year bonds to yield 8% on January 1, 2009. Interest is paid on June 30 and December 31. The proceeds from the bonds are Php 4,901,036. Using straight-line amortization, what is the carrying value of the bonds on December 31, 20 11? a. Php 4,917, b. Php 4,985, c. Php 4,908, d. Php 4,915,

A company issues Php 5,000,000, 7%, 20-year bonds to yield 8% on January 1, 2010. Interest is paid on June 30 and December 31. The proceeds from the bonds are Php 4,901,036. What is interest expense for 20 11 , using straight-line amortization? a. Php 385, b. Php 390, c. Php 392, d. Php 394,

Intermediate Accounting: Contingent Liability and Bonds payable

Course: Intermediate accounting (ACC 205)

University: Batangas State University