- Information

- AI Chat

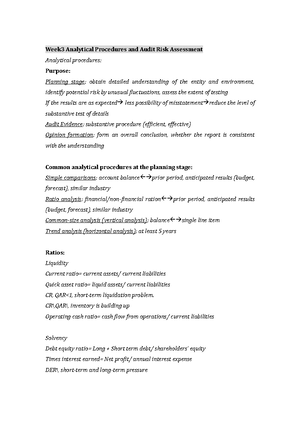

Accg3040 week 4

Auditing and Assurance Services (ACCG340)

Macquarie University

Recommended for you

Preview text

Tutorial Week 4

Audit Risks have three elements being:

Inherent Risk (nature of the business)– Arises because of the nature of the business or company. i. Company that’s works with predominately with cash or jewellery. Inherent risks come before control risk. These risks are before internal controls are implemented. Inherent risks before any internal controls are implemented. Auditors can only asses inherent risk, not change inherent risk -> look to keep it as a minimum

Control – Risk the company’s internal controls do not work effectively or prevent fraud. Auditors assess control risks. If they are not operating effectively, at the end of the audit they have to give suggestion to management on how to improve the internal controls.

Detection – Won’t be able to detect material risk statements. Determined by the auditor. Failed to detect material misstatement. Audits can change the risks by selecting more samples.

If inherent risk and control risks are high, the auditor will have to lower these risks by selecting more samples for testing. Auditor needs to apply more audit procedures

Business risk – affects the whole financial statements i. Cost of fuel increases expenditure and affects profitability of the whole company. Business risk is also when a whole company shuts down due to a lockdown.

Versus inherent risk where inventory gets stolen i. Clothes, where inventory balance is affected but won’t change the sales and net profit balance.

Higher detection risk means inherent and control risks are low, meaning the auditors can test less. Vice versa

When risk of material misstatements is likely to occur – auditor’s will set a lower threshold for materiality. Vice versa. i. Poor internal controls lower threshold, good internal controls higher materiality threshold.

Misappropriation of assets – Stealing items

Accg3040 week 4

Course: Auditing and Assurance Services (ACCG340)

University: Macquarie University