- Information

- AI Chat

Econ 101 Exam 1 Cheat Sheet

Principles of Economics I (Econ 101)

University of Michigan

Recommended for you

Preview text

Vocab:

- Models: simplifications to understand complex situations and draw conclusions of cause and effect

- Ceteris Paribus assumption: all else equal Concepts:

- Circular Flow Model a. Households, markets, firms, factor markets b. 2 agents,2 markets c. Does not account for saving → assumes that all money is spent d. Does not account for the fact that people get paid a different amount for labor

- Models a. The point of models is to make positive statements about the world b. Positive statements are objective facts (can be incorrect) c. Developed in support of normative claims → what ought to be d. Make positive statements to make normative statements e. Models work by making logical statements based on assumptions f. If then statements

- Opportunity cost a. The value of the next-best option b. A measure of the value of the choice you made, rather than the value of what you gave up c. Economic cost

- Economic costs a. The total value of what’s given up to make some choice

- Accounting costs a. Explicit costs → money outlays required to make a choice

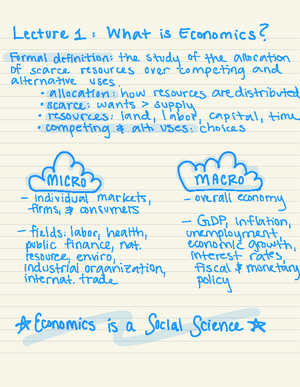

- Economics a. Study of choice where we have unlimited wants and scarce resources (constrained choices)

- Either-or decision a. Sometimes called the extensive margin b. Picking one option out of many

- Either-or decision principle a. Always make the choice that has positive economic profit b. Every choice but the best has negative economic profit

- How much decision a. Sometimes called the intensive margin b. Given either-or, how much do you do of that thing

- Cost-benefit analysis a. Rational person makes the choice that maximizes net benefits given:

i. All the options and information they are aware of ii. The value they attach to all of their options iii. The economic costs of all their options iv. All of the constraints they face 11. Net Benefit a. The value of its benefits minus the value of its economic costs 12. Economic profits a. Measurement of net benefits 13. Marginal value a. Change in total value 14. Marginal a. The change in a value when you increase or decrease in activity 15. Marginal benefits a. The change in total benefits from one or more unit of a good b. Derivative of a total benefit curve 16. Law of Diminishing Marginal benefits a. Also called the law of diminishing returns or law of decreasing MBs b. In many situations, there are diminishing marginal benefits to economic activity 17. Marginal costs a. Change in total cost from one or more unit of a good b. Derivative of total cost curve c. Increase over time → total costs increase exponentially 18. Net marginal benefit a. Marginal benefit - marginal cost 19. Maximizing economic profits a. Called the optimal quantity b. MB = MC 20. Equilibrium a. Point where if no relevant factors change, we will remain at that point b. MC = MB 21. Stable Equilibrium a. Equilibrium where if were not at that state, were going to move towards it 22. Utility a. The goodness of a transaction b. Utility is an economic value c. Measured in utils 23. Total Utility Function Laws a. More is better (satiation) i. TU slopes upwards, MU is positive b. Diminishing marginal utility i. MU has negative slope ii. Slope of TU falls as Q rises 24. Budget Constraint a. Describes what a household can afford

b. Assume diminishing marginal productivity 39. Marginal product of labor a. Change in the output when we increase the quantity of labor 40. Marginal Profit a. MP = MR - MC b. When MP is positive, increase production 41. Average profit a. Profit divided by number of units 42. Average costs a. AFC always declines b. AVC grows exponentially because of diminishing marginal productivity of labor c. As quantity increases, AVC gets closer to ATC d. ATC starts high, dips, then grows (parabolic) 43. Firm Supply Curve a. Optimal quantity produced by P = MC b. “Willingness to produce” c. As P rises, Q rises d. As P falls, Q falls 44. Shutdown price a. Point where MC intersects the AVC curve b. Price where production is no longer profit-maximizing c. Prices above shutdown → better profits d. Firms are willing to produce at any price on the MC curve above AVC e. MC above AVC is the firm relationship between price and optimal quantity 45. Firm Supply Curve a. Relationship between a goods price and one firms optimal production, holding fixed costs constant b. MC curve above AVC, the shutdown price 46. Supply and demand model a. Determines the price of a good and how much of that good is produced in a competitive market 47. Perfect competition a. Classic idea of the free market b. Central assumption is that firms and households are all price takers c. Production and prices are determined by economic fundamentals 48. Price taker a. Take the price as given b. The assumption of price taking means that choices are independent 49. Independence a. Government controls and actions b. Other consumers c. Other firms 50. Economic fundamentals a. Consumer preferences

b. Firm production technologies (production function) c. The resources available to households and firms 51. Market independence a. There are many firms i. No single firm has a large market share ii. Free entry to the market b. The is no product differentiation 52. Market demand curve a. The market demand curve is the relationship between market price and the optimal consumption of all households in the market b. Market demand gives the total willingness to pay for a certain quantity 53. Demand schedule a. Table containing information of demand curve 54. Law of Demand a. As P rises, QD falls b. P α1/Q 55. Market supply curve a. Relationship between market price and optimal production of all firms in the market b. As P rises, QS rises 56. Market Equilibrium a. Point where demand meets supply curve b. Only price where QD = QS c. Stable equilibrium d. Past equilibrium, additional units have negative MP 57. Market Clearing Price a. The intersection of supply and demand determines the market price, and at that price households and firms produce and consume the same amount 58. Excess demand a. The amount by which quantity demanded exceed quantity supplied (QD - Qs) when the price causes QD>Qs 59. Excess Supply a. The value QS - QD when price causes QS>QD 60. Market Price a. Measuring stick of value i. Price reflects willingness to pay b. Allocation mechanism i. Allocates goods according to willingness to pay

Graphs

- Total cost is generally concave up and increasing a. Marginal cost increases

Graphs:

Circular Flow Model: Total Benefits:

Marginal Benefits: Total Costs:

Total Economic Profits: Total Utility and Marginal Utility

Budget Line: Total Utility Function: Indifference Curves:

Total Product Marginal Product Marginal and Total product

Total Cost Marginal Cost

Firm Supply Curves:

Market Demand Curve: Market Supply Curve: Supply and Demand Curves

Econ 101 Exam 1 Cheat Sheet

Course: Principles of Economics I (Econ 101)

University: University of Michigan

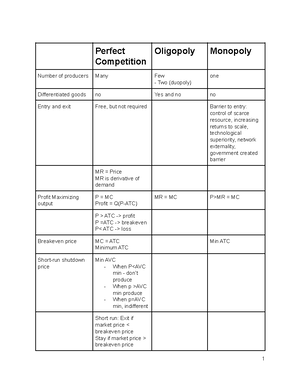

- Discover more from: