- Information

- AI Chat

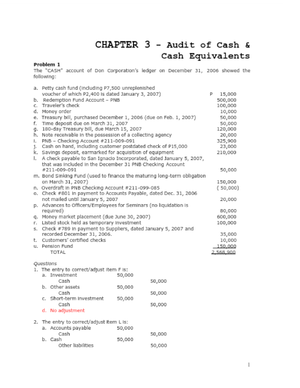

01-28-2022-crc-ace-afar-week-01-accounting-for-partnership-part-1-formation compress

Accounting (ACTG 100)

STI West Negros University

Recommended for you

Students also viewed

Related documents

- SOL - Chapter 6 Employee Benefits solution manual millan

- Tanginan C Ass Pricing and Profitability Analysis

- Hope q3-4 mod7 sportseventforatargethealthissueorconcernfootball v2

- Q4 Applied Filipino-Piling-Larang-Akad 12 wk8

- Doc1 - it was rightful to use so used it's as much as you can.

- Accounting 101 A 9 quiz - practice

Related Studylists

AFPreview text

ADVANCED FINANCIAL ACCOUNTING & REPORTING PROF. ROEL E. HERMOSILLA

WEEK 1 - ACCOUNTING FOR PARTNERSHIP

PARTNERSHIP FORMATION

There are no authoritative pronouncements concerning the accounting for partnership. The principles described have evolved through accounting practice.

Partnership Formation The partnership is a separate accounting entity (not to be confused with a separate legal entity), and therefore its assets and liabilities should remain separate and distinct from the individual partner’s personal assets and liabilities.

All assets contributed to the partnership are recorded by the partnership at their fair market values. All liabilities assumed by the partnership are recorded at their present values.

Upon formation, the amount credited to each partner’s capital account must be equal to the amount of cash contributed or equal to the fair market value of the noncash contributed or equal to the difference between the fair market value of the assets (including goodwill, if any) contributed and the present value of the liabilities assumed from the partner. The capital accounts represent the residual equity of the partnership. The capital account of each partner reflects all of the activity of an individual partner; contributions, withdrawals, and the distributive share of net income (loss). In some cases, a drawing account is used as a clearing account for each partner’ transactions with only the net effect of each period’s activity shown in the capital account.

Example: Partnership Formation A and B form a partnership. A contributes cash of P50,000, while B contributed land with a fair market value of P50,000 and the partnership assumes a liability on the land of P25,000.

The entry to record the formation of the partnership is Cash P50, Land 50, Liabilities P 25, A, capital 50, B, capital 25,

Sometimes, a partner will contribute intangible benefit to the partnership like good management skills, good business reputation, business connections, or anything that will bring in higher income to the business. The partners may agree to quantify this in the form of either goodwill or bonus.

Example: C and D agreed to form a partnership, with C contributing P100,000 cash and D contributing P150,000 cash. The partners agreed that C will also contribute an intangible benefit to the business for C to have an initial equal interest in the partnership.

If the bonus method is to be used, the entry in the partnership books must be: (1) To record the initial contribution of partners: Cash P250, C, Capital P100, D. Capital 150,

(2) To record the bonus recognized: D, Capital P25, C, Capital P25,

TThhee PPrrooffeessssiioonnaall CCPPAA RReevviieeww SScchhooooll

Davao 3/F GCAM Bldg. Monteverde St. Davao City 0917-

Baguio 2 nd Flr. #12 CURAMED Bldg. Marcos Highway, Baguio City 0906-0775156 / 09618683385

Main: 3F C. Villaroman Bldg. 873 P. Campa St. cor Espana, Sampaloc, Manila (02) 8735 8901 / 0917- email add: crc_ace@yahoo.com/crcacemanila@gmail

If the goodwill method is to be used, the entry in the partnership books must be: (1) To record the initial contribution of partners: Cash P250, C, Capital P100, D. Capital 150, (2) To record the goodwill recognized: Goodwill P 50, C, Capital P50,

The use of either method must be explicitly stated in the problem, otherwise the use of bonus method is preferable over goodwill method. Sometimes, two or more single proprietorships may wish to combine their businesses and agree to form a partnership. In this case, the assets and liabilities of the sole proprietors are normally restated or revalued to their fair values in order to adjust their capital accounts prior to recording their contributions in the partnership books. The restated or revalued capitals are now the partners’ initial contribution.

Example: Jackson and Johnson decided to form a partnership on January 3, 202B, to be called the JJ Merchandising. The following are their respective balance sheets immediately before the formation: Jackson Store Balance Sheet December 31, 202A Assets Liabilities and Capital Cash P130,000 Accounts Payable P125, Accts. Receivable 100,000 Jackson, Capital 355, Merchandise Inventory 200, Furniture 50,000 _______ Total P 480,000 Total P480,

Johnson Store Balance Sheet December 31, 202A

Assets Liabilities and Capital Cash P 15,000 Accounts Payable P 15, A/R P40,000 Notes Payable 20, Less: ADA 4,000 36,000 Johnson, Capital 79, Merchandise Inventory 50, Furniture P15, Less: A/D 1,500 13,500 _______ Total P114,500 P114,

The two partners agree to the following adjustments: 1. That P20,000 of Jackson’s accounts receivable be written off. 2. That Jackson’s furniture has a market value of P40,000. 3. That accrued expenses of P25,000 be recognized on Jackson’s books. 4. Johnson’s estimated uncollectible accounts should be 5% of the outstanding accounts receivable. 5. The fair value of Johnson’s furniture is P12,000. 6. Total partners’ equity should be P400,000 with Jackson’s interest representing 75%. The most likely question will be how much capital must be recorded in the partnership books. Then your answer must be P300,000 for Jackson and P100,000 for Johnson. The partnership balance sheet immediately after its formation will be presented as follows: JJ Merchandising Balance Sheet January 3, 202B

Assets Liabilities and Capital Cash P145,000 Accounts Payable P 140, Accts. Rec. 120,000 Notes Payable 20,00 0 Less: ADA 2,000 118,000 Accrued Expenses 25, Merchandise Inventory 250,000 Jackson, Capital 300, Furniture 52,000 Johnson, Capital 100, Goodwill 20,000 ________ Total P 585,000 P 585,

obsolete apparatus acquired for P96,000 with an accumulated depreciation balance of P84,000. Part of the intangibles is a patent with a carrying value of P14,000 which was sued upon by a competitor. Paul unsuccessfully defended the case and the final decision of the court was released on February 12, 202A. What is the fair value of the equipment invested by Allan? A. P242, B. P336, C. P350, D. P390,

- Scarlett and Natalie decided to form a partnership on May 1, 202A. The assets to be contributed by the partners are: Scarlett Natalie Book Value Fair Value Book Value Fair Value Cash P375,000 P375,000 P875,000 P875, Merchandise inventory 95,000 125, Furniture and fixtures 350,000 312,500 872,500 937, Transportation equipment 3,262,500 2,812,

The transportation equipment is subject to a mortgage loan of P1,125,000, which is to be assumed by the partnership. The partnership agreement provides that Scarlett and Natalie share profits and losses of 30% and 70% respectively. Assuming that the partners agreed to bring their respective capital in proportion to their profit and loss ratio, using Natalie capital as base, how much additional cash is to be invested (withdrawn) by Scarlet? A. P687, B. P875, C. (P987,500) D. (P687,500)

- The balance sheet as of July 31, 202A for the business owned by Angelina, shows the following assets and liabilities: Cash P 110,000 Fixtures P 360, Accounts Receivable 294,800 Accounts Payable 63, Merchandise 484, It is estimated that 5% of the receivable will prove uncollectible. The cash balance includes 1, share certificates of PNB at its cost, P 8,000; the stock last sold on the market at P 70 per share. Merchandise includes obsolete items costing P 36,000 that will probably realize only P 8,000. Depreciation has never been recorded; the fixtures are 2 years old, have an estimated life of 10 years, and would cost P 480,000 if purchased new currently. Sundry prepaid items amount to P 10,000. Danny is to be admitted as a partner upon investing P 400,000 cash and P 200, merchandise.

What will be the total capital after the formation of partnership?

- Emma and Shailane establish a partnership to operate to a used-furniture business under the name Amorini Furniture. Emma contributes furniture that cost P 78,000 and has a fair value of P 117,000. Shailane contributes to P 39,000 cash and delivery equipment that cost P 52,000 and has a fair value of P 39,000. The partners agree to share profits and losses 60% to Emma and 40% to Shailane.

Calculate the peso of inequity that will result if the initial noncash contributions of the partners are recorded at cost rather than fair market value.

- The balance sheet of the proprietorship of Margot as of June 30, 202A showed the following assets and liabilities: Cash P 48, Accounts Receivable 64, Inventory 105, Equipment 78, Accounts Payable 76,

The cash balance included a 200-share certificate of CW Resources common at acquisition cost of P 1,600; the current market quotation is P 70 per share. Of the accounts receivable, an estimated

5% is considered to be doubtful of collection. Certain inventory items, booked at cost of P 22,960, are currently worth P 16,000. Depreciation has not been recorded; the equipment, acquired two years ago, has a remaining useful life of about eight more years. Prepaid expense of P 12,800 and accrued expense of P 6,120 have not been properly recognized. Jessica and Kirsten will join Margot in a partnership. Margot will invest the net assets of her business, after effecting the appropriate adjustments, and she will be allowed credit for goodwill equal to 10% of her initial capital credit.

Jessica and Kirsten will each contribute cash to secure the respective interests of 1/3 and 1/6, respectively. A. Margot’s goodwill credit would be: B. Jessica’s cash investment would be:

- Anna and Salve are partners sharing profits 60:40. A balance sheet prepared for the partnership on April 1, 2018 shows the following: Cash 48,000 Accounts Payable

89,

Accounts Receivable 92,000 Anna, Capital 133, Inventory 165,000 Salve, Capital 108, Equipment 70, Accumulated depreciation

(45,000)

330,000 330,

On this date, the partners agree to admit Connie as a partner. The terms of the agreement is that assets and liabilities are to be restated as follows: a. An allowance for possible uncollectible Salve of P4,500 is to be established b. Inventories are to be restated at their present replacement values of P170, c. Equipment are to be restated at a value of P35, d. Accrued expenses of P4,000 are to be recognized

Anna, Salve, and Connie will divide profits in the ratio of 5:3:2. Capital balances for the new partners are to be in this ratio with Anna and Salve making cash settlement outside of the partnership for the required capital adjustment between themselves and Connie investing cash in the partnership for her interest.

Questions: 1. How much cash Connie should contribute? 2. How will you state the settlement between Anna and Salve? 3. Journal Entries to reflect the above transactions.

reh/cde

01-28-2022-crc-ace-afar-week-01-accounting-for-partnership-part-1-formation compress

Course: Accounting (ACTG 100)

University: STI West Negros University

This is a preview

Access to all documents

Get Unlimited Downloads

Improve your grades

Why is this page out of focus?

Students also viewed

Related documents

- SOL - Chapter 6 Employee Benefits solution manual millan

- Tanginan C Ass Pricing and Profitability Analysis

- Hope q3-4 mod7 sportseventforatargethealthissueorconcernfootball v2

- Q4 Applied Filipino-Piling-Larang-Akad 12 wk8

- Doc1 - it was rightful to use so used it's as much as you can.

- Accounting 101 A 9 quiz - practice